Gallagher Update:

Gallagher Update:

Global insurance losses from the Russia-Ukraine war could range from USD 16 billion to USD 35 billion, with reinsurers expected to assume 50% of those claims, according to a report published by S&P Global Ratings1. There are currently some 515 aircraft leased to Russian airlines with an appraised insured value of USD 12 billion, with only 78 aircraft having been reported as safely recovered. Indeed earlier this month the world’s largest aircraft lessor announced it has submitted a USD 3 billion claim to its insurers. Beyond aviation, other classes of insurance are also exposed, including trade credit (contract frustration, agriculture and commodities), political violence and marine hull war. Nevertheless, S&P has said the reinsurance sector’s annual expected pre-tax profit of about USD 22.5 billion, coupled with the natural catastrophe budget of about USD 13 billion, should provide a sufficient buffer to absorb these losses.

Although the financial institution insurance market is not directly exposed to insurance losses as a result of the war, it’s worth noting that many financial institution insurers also insure the classes of insurance that are likely to be impacted. As such, if the losses are particularly severe it is possible that there could be some upward impact on the financial institutions market. However, at this stage, Gallagher believes that is a remote possibility, predominantly because the potential quantum is not sufficient to shift the entire market place.

Beyond that, Gallagher are seeing many financial institution insurers react to developments by adding a specific territorial restriction exclusion to policies. In short, this excludes coverage for any entities, individuals or property located in Russia or Belarus and also excludes claims brought or maintained in those countries. Gallagher are also aware that Cyber insurers are introducing updated war exclusions to their policies. In some cases, this may result in no cyber coverage applying in the event of a state sponsored cyber-attack by Russia. Further, most insurers are now asking specific questions around Russia at renewal, such as whether the insured has any exposure to designated persons or politically exposed persons with a nexus to Russia, Ukraine or Belarus and the controls and procedures in place to ensure that future sanction changes are acted upon. Financial Institutions that have a material exposure should expect a challenging renewal and may struggle to secure capacity.

These are clearly issues that need to be navigated with care and we will provide assistance on what needs to be disclosed and the manner in which the information is dissipated.

If you would like to discuss the implications of these developments with us, please get in touch with Peter O’Donnell.

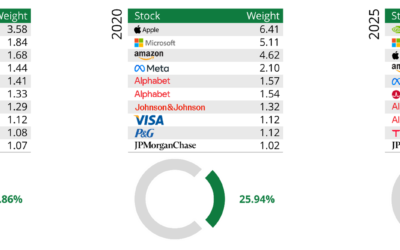

Quilter update | September 2025

The dollar dilemma: combatting hidden risks Despite ongoing political uncertainty and a sharp decline in the value of the dollar, US equities have continued their upward trajectory, hitting new all-time highs. However, some multi-asset investment...

MAC Golf Day 2025

MAC Group is proud to announce that an incredible £14,500 was raised for Forget Me Not at this year’s MAC Golf Day.

Quilter Cheviot | Investment review of Q2 and H1 2025

Olly Smith, Investment Manager summarises what has happened in the second quarter of 2025, and the impact of Trump’s tariffs.

Procrastinating may cost you dearly

Why procrastinating may cost you dearly By Natalie Bush, Senior Independent Financial Adviser (IFA)We all lead busy lives, and it’s easy for long-term planning to be pushed aside by day-to-day priorities. But when it comes to your financial future,...

MAC Group Sponsors IOM Swim Team

MAC Group is proud to have supported the Isle of Man Swim Team as Silver Sponsor for the 2025 Island Games in Orkney.

Insurance market update Summer 2025

Ann Zachorecki highlights rising costs, regulation, and talent gaps shaping the UK and Isle of Man insurance landscape.

Saving for university?

Senior IFA, John Condon explores the help available for Manx students going to university and the financial impact on families.

Colin Moore Joins MAC Financial

MAC Financial is pleased to announce the appointment of Colin Moore PhD, Chartered FCSI, as a Senior Independent Financial Adviser.

Ed Walter appointed MD of MAC Financial Limited

MAC Group is delighted to announce the promotion of Ed Walter to Managing Director of MAC Financial.